Short-term health insurance policies set the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail and brimming with originality from the outset. Delving into the world of short-term health insurance, we uncover the nuances of coverage, costs, and the application process, providing a comprehensive guide for those seeking temporary health insurance solutions.

Overview of Short-term Health Insurance Policies

Short-term health insurance policies are designed to provide temporary coverage for individuals who are in transition periods, such as between jobs or waiting for employer-sponsored benefits to kick in. These policies typically offer coverage for a limited duration, ranging from a few months to a year.

Purpose of Short-term Health Insurance

Short-term health insurance policies are meant to bridge the gap between coverage periods, offering protection in case of unexpected medical expenses during transitional periods. They are a cost-effective option for individuals who need temporary coverage and do not want to commit to a long-term plan.

- Short-Term vs. Long-Term Plans:

Short-term health insurance policies differ from long-term plans in terms of coverage duration and benefits. While long-term plans offer comprehensive coverage for an extended period, short-term policies provide limited coverage for a temporary period.

Examples of Situations where Short-term Policies are Useful

Short-term health insurance policies can be useful in various situations, including:

- Individuals in between jobs

- Recent college graduates waiting for employer benefits

- Early retirees who do not yet qualify for Medicare

- Individuals aging out of their parents’ insurance

Coverage and Limitations

When it comes to short-term health insurance policies, coverage and limitations play a crucial role in understanding the extent of benefits and restrictions provided. Let’s delve into what short-term health insurance typically covers and the common limitations or exclusions you may encounter.

Coverage

Short-term health insurance policies generally cover basic medical services, such as doctor visits, emergency care, hospitalization, and prescription drugs. These policies are designed to provide temporary coverage for individuals in between traditional health insurance plans or during life transitions, such as job changes or early retirement. However, it’s important to note that coverage can vary depending on the specific policy and insurance provider.

- Doctor visits

- Emergency care

- Hospitalization

- Prescription drugs

Limitations and Exclusions, Short-term health insurance policies

Despite the coverage provided by short-term health insurance policies, there are common limitations and exclusions to be aware of. Pre-existing conditions are often not covered under these policies, meaning any medical conditions you had before purchasing the policy may not be covered. Additionally, preventive care, maternity care, mental health services, and substance abuse treatment may also be excluded from coverage.

- Pre-existing conditions

- Preventive care

- Maternity care

- Mental health services

- Substance abuse treatment

Situations Where Coverage May Not Apply

It’s important to understand that there are situations where coverage under a short-term health insurance policy may not apply. For example, if you seek treatment for a condition that is not covered by the policy, you may be responsible for paying the full cost out of pocket. Additionally, if you receive care from a provider that is out of network, your policy may not cover the expenses, leaving you with a significant financial burden.

- Seeking treatment for a non-covered condition

- Receiving care from an out-of-network provider

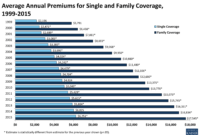

Cost and Affordability

When it comes to short-term health insurance, understanding the cost and affordability is crucial for making an informed decision. Let’s dive into how the cost of short-term health insurance is calculated, compare the affordability of short-term plans to traditional health insurance, and provide tips for finding the most cost-effective short-term policy.

Cost Calculation

Short-term health insurance premiums are typically calculated based on various factors such as age, location, coverage options, and duration of the policy. Generally, younger individuals with fewer pre-existing conditions may pay lower premiums compared to older individuals with more health issues. Additionally, the coverage level and deductible amount chosen can also impact the overall cost of the policy.

Affordability Comparison

Short-term health insurance plans are often more affordable than traditional health insurance plans, especially for individuals who are in good health and do not require extensive coverage. While short-term plans may have lower monthly premiums, it’s important to note that they may also have limitations on coverage and benefits compared to comprehensive health insurance plans. Therefore, affordability needs to be balanced with the level of coverage needed to ensure adequate protection.

Tips for Finding Cost-Effective Policies

- Compare multiple insurance providers to find the best rates and coverage options.

- Consider a higher deductible to lower monthly premiums, but make sure you can afford the out-of-pocket costs if needed.

- Look for short-term plans with customizable coverage options that align with your healthcare needs.

- Review the policy details carefully, including coverage exclusions, limitations, and renewal options.

- Consult with an insurance agent or broker to help you navigate the complexities of short-term health insurance and find the most cost-effective policy for your situation.

Application Process and Duration

When applying for a short-term health insurance policy, the process is typically straightforward and can often be completed online. Applicants are usually required to provide personal information such as age, address, and medical history. Some insurers may also require a brief medical exam or questionnaire.

Duration of Coverage

Short-term health insurance plans typically provide coverage for a limited duration, usually ranging from 30 days to 364 days, depending on the state regulations. It’s important to note that these plans are not renewable in some states, and policyholders may need to reapply for a new plan once the current one expires.

Renewing or Extending Policies

Renewing or extending short-term health insurance policies can vary depending on the insurer and state regulations. In some cases, policyholders may be able to renew their plan for an additional term, but this is not always guaranteed. It’s essential to check with the insurer regarding the options available for extending or renewing a short-term health insurance policy.

In conclusion, Short-term health insurance policies offer a flexible and temporary solution for individuals in need of immediate coverage. Understanding the intricacies of coverage, costs, and the application process is essential for making informed decisions regarding short-term health insurance. Whether it’s bridging a gap in coverage or exploring cost-effective options, short-term policies provide a valuable resource in the ever-evolving landscape of healthcare.

When it comes to choosing the right health insurance plan, understanding the differences between a High deductible health plan (HDHP) and other options is crucial. HDHPs typically offer lower monthly premiums in exchange for higher deductibles, making them a popular choice for those who are generally healthy and don’t anticipate many medical expenses.

For self-employed individuals, finding the right health insurance plan can be challenging. It’s important to consider factors like coverage options, costs, and network providers. Working with an insurance broker can help navigate the complexities of healthcare options and find a plan that meets individual needs.

Choosing between a PPO and HMO health insurance plan involves understanding the differences in network coverage and out-of-pocket costs. PPOs offer more flexibility in choosing healthcare providers, while HMOs require referrals for specialists. Consider personal healthcare needs and budget when deciding between the two.

{kind=link}