How to choose health insurance coverage takes center stage in this detailed guide, offering valuable insights and practical tips for navigating the complex world of healthcare options. From understanding key factors to comparing cost considerations, this article equips you with the knowledge needed to make informed decisions about your health coverage.

Explore the essential components of selecting the right health insurance plan and empower yourself to prioritize your well-being with confidence.

Factors to Consider

When choosing health insurance coverage, there are several important factors to consider in order to determine the most suitable plan for your needs.

Cost

- Monthly premiums

- Deductibles

- Copayments and coinsurance

Understanding the overall cost of the plan is crucial to ensure it fits within your budget.

Coverage and Benefits

- Services covered

- Prescription drug coverage

- Mental health coverage

Checking what services are included in the plan can help you determine if it meets your specific healthcare needs.

Network

- In-network providers

- Out-of-network coverage

- Referral requirements

The size and quality of the provider network can impact your access to healthcare services and the cost of care.

Customer Service

- Accessibility and responsiveness

- Complaint resolution process

- Online tools and resources

Having access to good customer service is essential in case you have questions or issues with your coverage.

Reputation and Financial Stability

- Company ratings

- Financial strength

- Claims processing efficiency

Choosing a reputable insurance provider with a strong financial standing can give you peace of mind that your claims will be processed efficiently.

Types of Health Insurance Plans

Health insurance plans come in various types, each offering different levels of coverage, costs, and flexibility. Understanding the key features and differences between these plans can help you choose the right one for your needs.

Health Maintenance Organization (HMO) Plans

HMO plans typically require you to choose a primary care physician (PCP) and get referrals to see specialists. These plans often have lower out-of-pocket costs but limit your choice of healthcare providers.

- Key Features: PCP coordination, network restrictions

- Benefits: Lower premiums, predictable costs

- Limitations: Limited provider choices, referrals required

Preferred Provider Organization (PPO) Plans

PPO plans offer more flexibility in choosing healthcare providers and do not require referrals to see specialists. While premiums may be higher, you can see out-of-network providers at a higher cost.

- Key Features: Provider network, out-of-network coverage

- Benefits: Provider choice, no referrals needed

- Limitations: Higher premiums, out-of-network costs

Exclusive Provider Organization (EPO) Plans

EPO plans combine features of HMO and PPO plans, offering a provider network like an HMO but without requiring referrals. However, coverage is typically limited to in-network providers only.

- Key Features: In-network coverage, no referrals needed

- Benefits: Lower costs, no out-of-network coverage

- Limitations: Limited provider choices, in-network restrictions

Point of Service (POS) Plans

POS plans allow you to choose between in-network and out-of-network care, similar to PPO plans. You may need to select a PCP and get referrals for specialist care, blending features of HMO and PPO plans.

- Key Features: In-network and out-of-network options, PCP coordination

- Benefits: Flexibility in provider choice, out-of-network coverage

- Limitations: Referrals may be required, higher out-of-pocket costs

Coverage Options

When selecting a health insurance plan, it is crucial to understand the different coverage options available to ensure that your healthcare needs are adequately met. Each coverage option plays a significant role in determining the extent of care you receive and how much you may need to pay out of pocket.

Preventive Care

- Preventive care services include routine check-ups, vaccinations, screenings, and counseling to prevent illness or detect conditions early.

- Understanding the coverage for preventive care can help you stay proactive about your health and potentially avoid more serious health issues down the line.

Prescription Drugs

- This coverage option pertains to the medications prescribed by your healthcare provider to manage or treat various health conditions.

- Knowing the coverage for prescription drugs can impact your out-of-pocket costs significantly, as some plans may require copayments or coinsurance for certain medications.

Mental Health Services

- Mental health services encompass therapy, counseling, and treatment for mental health conditions such as anxiety, depression, or substance abuse.

- Understanding the coverage for mental health services is essential for accessing the care you need to maintain your mental well-being.

Assessing Personal Healthcare Needs

- Consider your current health status, any chronic conditions, and anticipated medical needs when determining the coverage options you require.

- Reviewing your medical history and consulting with healthcare providers can help you identify the essential coverage options that align with your healthcare needs.

Impact on Out-of-Pocket Costs, How to choose health insurance coverage

- The coverage options you select can directly impact the amount you pay out of pocket for medical services, including copayments, coinsurance, and deductibles.

- Choosing coverage options that align with your healthcare needs can help you manage your out-of-pocket costs effectively and ensure you receive the necessary care without financial burden.

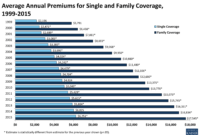

Cost Considerations: How To Choose Health Insurance Coverage

When choosing health insurance coverage, understanding the cost implications is crucial. Various factors contribute to the overall cost of health insurance, including premiums, deductibles, co-pays, and coinsurance. It is essential to consider these factors carefully to ensure that you select a plan that meets your healthcare needs while remaining affordable.

Premiums

Premiums are the fixed amount you pay each month to maintain your health insurance coverage. Higher premiums often indicate more comprehensive coverage, while lower premiums may come with higher out-of-pocket costs when you receive care. It’s essential to strike a balance between premiums and out-of-pocket expenses to find a plan that fits your budget.

Deductibles and Co-pays

Deductibles are the amount you must pay out-of-pocket before your insurance starts covering costs. Co-pays are fixed amounts you pay for specific services, such as a doctor’s visit or prescription medication. Understanding these costs helps you anticipate your financial responsibility for healthcare services throughout the year.

Coinsurance and Cost-sharing

Coinsurance is the percentage of costs you share with your insurance provider after meeting your deductible. Cost-sharing refers to the division of healthcare costs between you and your insurer. By knowing how coinsurance and cost-sharing work, you can estimate your out-of-pocket expenses for medical services and treatments.

Comparing Costs

To find the most cost-effective health insurance plan, compare the total costs, including premiums, deductibles, co-pays, and coinsurance, across different options. Consider your typical healthcare needs and expenses to determine which plan offers the best value for your money. Pay attention to network coverage, prescription drug coverage, and additional benefits when evaluating costs.

Balancing Costs with Coverage

While cost is a significant factor in choosing health insurance, it’s essential to balance costs with coverage. Opting for the cheapest plan may leave you underinsured, leading to higher out-of-pocket expenses in the long run. Evaluate your healthcare needs, budget, and desired benefits to strike a balance between affordability and comprehensive coverage.

In conclusion, choosing the right health insurance coverage is a crucial decision that requires careful consideration and understanding. By weighing various factors, exploring different plan types, and evaluating coverage options, you can secure a plan that meets your needs effectively. Remember, your health is an investment worth protecting, so choose wisely.

Health insurance for emergency services is crucial for individuals to ensure they receive timely and quality care in case of unexpected medical needs. Having the right coverage can provide peace of mind and financial protection during emergencies. To learn more about the importance of health insurance for emergency services, check out this informative article on Health insurance for emergency services.

Private health insurance for individuals offers personalized coverage options tailored to specific healthcare needs. This type of insurance provides access to a network of healthcare providers and facilities, ensuring timely and comprehensive medical care. To explore the benefits of private health insurance for individuals, read this detailed guide on Private health insurance for individuals.

High deductible health plans (HDHP) are becoming increasingly popular due to their lower monthly premiums and tax advantages. These plans require individuals to pay a higher deductible before insurance coverage kicks in, but they can be cost-effective for those in good health. To understand more about high deductible health plans (HDHP) and their benefits, visit this insightful article on High deductible health plans (HDHP).

{kind=link}