How much does health insurance cost? This burning question lingers in the minds of many, seeking to unravel the complexities of healthcare expenses. As we delve into this topic, prepare to uncover the hidden truths behind the numbers and factors influencing the cost of staying insured.

From the different types of insurance plans to strategies for cost reduction, this exploration will equip you with the knowledge needed to navigate the realm of health insurance costs effectively.

Overview of Health Insurance Costs

Health insurance costs can vary based on several factors, including age, location, coverage level, and the type of plan chosen. Understanding these factors can help individuals make informed decisions about their health insurance options.

When it comes to health plans, coverage for outpatient services is a crucial aspect to consider. Outpatient services, such as doctor visits and minor procedures, are often included in health plans to ensure comprehensive care for individuals. Understanding the extent of coverage for outpatient services can help individuals make informed decisions about their healthcare needs. To learn more about coverage for outpatient services under health plans, you can visit this link.

Factors Influencing Health Insurance Costs

- The age of the individual plays a significant role in determining health insurance premiums. Generally, older individuals may have higher premiums due to a higher risk of health issues.

- Location also impacts health insurance costs, as healthcare expenses can vary by region. Urban areas may have higher healthcare costs compared to rural areas.

- The level of coverage chosen, such as a basic plan with limited coverage versus a comprehensive plan with more benefits, will affect the cost of health insurance.

Types of Health Insurance Plans and Cost Ranges

- Health Maintenance Organization (HMO): HMO plans typically have lower premiums but require individuals to use healthcare providers within a specific network. Costs can range from $200 to $500 per month.

- Preferred Provider Organization (PPO): PPO plans offer more flexibility in choosing healthcare providers but usually come with higher premiums. Costs can range from $300 to $700 per month.

- High-Deductible Health Plan (HDHP): HDHPs have lower premiums but higher deductibles. Costs can range from $150 to $400 per month.

Calculation of Insurance Premiums

Insurance premiums are calculated based on a combination of factors, including age, location, coverage level, and the type of plan selected. Insurers use actuarial tables and risk assessment to determine the appropriate premium for each individual.

For parents, pediatric care coverage under health insurance is essential for the well-being of their children. Health insurance plans often include coverage for pediatric services, such as vaccinations, check-ups, and treatments for illnesses. Having adequate pediatric care coverage can give parents peace of mind knowing that their children’s healthcare needs are taken care of. To explore more about pediatric care coverage under health insurance, you can check out this link.

Average Costs of Health Insurance

When it comes to health insurance costs, understanding the average premiums for individuals and families, as well as the differences between employer-sponsored and private health insurance plans, is crucial. Let’s delve into the details to see how these costs vary across different states or regions in the country.

Average Monthly Premiums

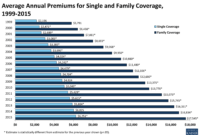

- The average monthly premium for an individual health insurance plan is around $440, according to recent data.

- For family coverage, the average monthly premium is approximately $1,168.

Employer-Sponsored vs. Private Health Insurance

- Employer-sponsored health insurance plans tend to have lower monthly premiums compared to private health insurance plans.

- On average, employees contribute about $118 per month towards their employer-sponsored health insurance, with employers covering the rest.

- In contrast, private health insurance plans can have higher monthly premiums, especially for comprehensive coverage.

Cost Variation by State

- The cost of health insurance can vary significantly depending on the state or region you reside in.

- States like Massachusetts and New Jersey typically have higher health insurance premiums due to state-specific regulations and healthcare costs.

- On the other hand, states like Utah and Iowa may have lower average premiums for health insurance.

Factors Affecting Health Insurance Premiums: How Much Does Health Insurance Cost?

:max_bytes(150000):strip_icc()/how-much-does-health-insurance-cost-4774184_V2-f7ab6efc9c5042d3aedcbc0ddfc6252f.png?w=700 "Insurance premium cost average premiums kff")

When it comes to health insurance premiums, there are several factors that can influence how much you pay for coverage. Understanding these factors can help you make informed decisions when selecting a health insurance plan.

Pre-Existing Conditions Impact, How much does health insurance cost?

Having pre-existing conditions can significantly impact your health insurance costs. Insurance companies may charge higher premiums or exclude coverage for certain conditions if you have a history of medical issues. It’s essential to disclose all pre-existing conditions when applying for health insurance to ensure you get the coverage you need.

Lifestyle Choices Influence

Lifestyle choices, such as smoking or lack of exercise, can also affect health insurance premiums. Individuals who engage in risky behaviors are considered higher risk by insurance companies, leading to higher premium costs. Making healthy lifestyle choices can not only improve your overall health but also reduce your insurance premiums in the long run.

Impact of Deductibles, Copayments, and Coinsurance

In addition to monthly premiums, deductibles, copayments, and coinsurance also play a significant role in determining your overall health insurance costs. Deductibles are the amount you pay out of pocket before your insurance kicks in, while copayments and coinsurance are the costs you share with the insurance company for covered services. Understanding these cost-sharing mechanisms can help you budget for healthcare expenses and choose a plan that aligns with your financial needs.

Strategies to Lower Health Insurance Costs

When it comes to reducing health insurance premiums, there are several strategies individuals can consider implementing. These strategies can help individuals save money while still ensuring they have the coverage they need.

Advantages and Disadvantages of High Deductible Health Plans

High deductible health plans (HDHPs) are a popular option for those looking to lower their health insurance costs. These plans typically have lower monthly premiums but come with higher deductibles. Here are some advantages and disadvantages to consider:

- Advantages:

- Lower monthly premiums compared to traditional plans.

- Opportunity to open a Health Savings Account (HSA) for tax savings.

- Encourages cost-conscious healthcare decisions.

- Disadvantages:

- Higher out-of-pocket costs before coverage kicks in.

- May not be the best option for those with chronic health conditions.

- Risk of delaying necessary medical care due to high deductibles.

Health Savings Accounts (HSAs) and Their Role in Cost Savings

Health Savings Accounts (HSAs) are tax-advantaged accounts that can be paired with HDHPs to help individuals save money for medical expenses. Here’s how HSAs work:

- Contributions to an HSA are tax-deductible, reducing taxable income.

- Funds in an HSA can be invested and grow tax-free.

- Withdrawals for qualified medical expenses are tax-free.

HSAs can be a valuable tool for saving on healthcare costs, as they offer a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses.

In conclusion, the realm of health insurance costs is multifaceted and ever-evolving. By understanding the various factors at play and exploring ways to mitigate expenses, individuals can make informed decisions about their healthcare coverage. Let this journey into the realm of health insurance costs empower you to take control of your financial well-being and overall health.

Emergencies can happen at any time, which is why having health insurance for emergency services is crucial. Health insurance plans typically cover emergency services, such as ambulance rides, emergency room visits, and urgent care treatments. Understanding the coverage for emergency services under your health insurance plan can help you be prepared for unexpected medical situations. To learn more about health insurance for emergency services, you can visit this link.

{kind=link}