Group health insurance cost for employees sets the stage for exploring the intricacies of factors, plan types, and cost-sharing mechanisms, offering a comprehensive guide to navigating this essential aspect of employee benefits.

Dive into the details to uncover valuable insights on managing costs effectively and ensuring both employers and employees make informed decisions regarding group health insurance.

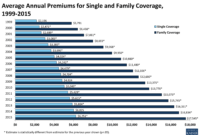

Factors influencing group health insurance cost

Group health insurance costs can be influenced by various factors that impact the overall premiums. Understanding these factors is crucial for employers looking to manage and mitigate rising costs.

When it comes to catastrophic health insurance plans, they typically cover major medical expenses after you reach a high deductible. This can include hospital stays, surgeries, and other serious medical treatments. However, routine care like check-ups and prescription drugs are usually not covered. To learn more about what is covered in catastrophic health insurance plans, you can check out this informative article: What is covered in catastrophic health insurance plans?

.

1. Number of Employees

The size of the employee group covered under the insurance plan plays a significant role in determining the cost. Larger groups may benefit from economies of scale, leading to lower premiums per employee.

For those looking for dental and vision insurance plans, there are options available to help cover the costs of routine dental and eye care. These plans can include coverage for cleanings, exams, glasses, and contact lenses. Understanding the details of these plans is important to ensure you have the coverage you need. To explore more about dental and vision insurance plans, you can refer to this comprehensive guide: Dental and vision insurance plans.

2. Age and Health Profile of Employees

The age and overall health of employees can impact insurance costs. Younger and healthier employees generally result in lower premiums, while older or less healthy employees may lead to higher costs.

3. Coverage Options and Benefits

The scope of coverage and the benefits offered in the insurance plan can affect costs. Comprehensive coverage with additional benefits will likely result in higher premiums compared to basic coverage options.

Alternative medicine such as acupuncture, chiropractic care, and herbal remedies are becoming more popular, but not all health insurance plans cover these treatments. Some plans may offer limited coverage or require additional riders for alternative therapies. To find out if your health insurance covers alternative medicine, it’s essential to review the policy details carefully. Learn more about this topic by reading: Does health insurance cover alternative medicine?

.

4. Location of the Business

The geographic location of the business can also influence insurance costs due to variations in healthcare costs and regulations. Areas with higher healthcare expenses may lead to increased premiums.

5. Claims History

The past claims history of the employee group can impact future insurance costs. A high frequency of claims or expensive medical treatments can lead to higher premiums as insurers assess the risk.

Strategies to Mitigate Rising Costs

- Implement wellness programs to promote employee health and reduce insurance claims.

- Shop around and compare quotes from different insurance providers to find the best rates.

- Consider adjusting coverage options or sharing costs with employees to manage expenses.

- Work with an insurance broker to negotiate better terms and explore cost-saving opportunities.

Types of group health insurance plans

When it comes to group health insurance plans for employees, there are several common types available. Understanding the differences between these plans can help employers and employees make informed decisions about coverage options.

HMOs (Health Maintenance Organizations)

- HMOs require employees to choose a primary care physician (PCP) from a network of providers.

- Employees must get referrals from their PCP to see specialists.

- Costs are typically lower for both employers and employees, but there is less flexibility in choosing healthcare providers.

PPOs (Preferred Provider Organizations)

- PPOs offer more flexibility in choosing healthcare providers, allowing employees to see specialists without referrals.

- Costs are higher compared to HMOs, both in terms of premiums and out-of-pocket expenses.

- Employers may have to pay higher premiums, but employees have more control over their healthcare choices.

EPOs (Exclusive Provider Organizations)

- EPOs combine elements of HMOs and PPOs, requiring employees to use a network of providers but not needing referrals for specialists.

- Costs for EPOs can vary, but they are often lower than PPOs and offer some flexibility in provider choice.

- Employers may benefit from cost savings compared to PPOs, while employees still have access to a network of providers.

Cost-sharing mechanisms in group health insurance

When it comes to group health insurance, cost-sharing mechanisms play a crucial role in determining the overall cost of the plan. These mechanisms include deductibles, copayments, and coinsurance, each impacting the financial responsibility of both the employer and employees.

Deductibles

Deductibles refer to the amount that employees must pay out of pocket before the insurance plan starts covering expenses. Higher deductibles typically result in lower premiums, making it an attractive option for employers looking to reduce costs. However, employees may face higher upfront expenses before reaching the deductible limit.

Copayments

Copayments are fixed amounts that employees pay for healthcare services, such as doctor visits or prescription drugs. By sharing the cost with employees, employers can lower their premium payments. Copayments provide predictability for employees but can add up over time, especially for those requiring frequent medical care.

Coinsurance, Group health insurance cost for employees

Coinsurance requires employees to pay a percentage of the total cost of healthcare services, even after meeting the deductible. This mechanism helps distribute costs between the insurance provider and the insured, reducing the financial burden on both parties. Employers can choose different coinsurance levels to balance premiums and out-of-pocket expenses for employees.

Cost-sharing mechanisms in group health insurance not only impact the overall cost of the plan but also influence how healthcare expenses are distributed between the employer and employees. By understanding these mechanisms and their implications, employers can design a cost-effective health insurance plan that meets the needs of their workforce.

Employee contributions to group health insurance: Group Health Insurance Cost For Employees

Employee contributions play a significant role in determining the cost of group health insurance. Let’s delve into how these contributions impact overall expenses, various cost-sharing arrangements, and effective communication strategies with employees regarding their financial responsibilities.

Impact of Employee Contributions

Employee contributions directly affect the cost of group health insurance plans. When employees contribute a portion of the premium, it reduces the financial burden on employers, ultimately leading to lower overall costs for the company.

- Employer and Employee Cost-Sharing

- Contributions can be set as a fixed amount or percentage of the premium

- Employees may also share costs through deductibles, copayments, or coinsurance

Cost-Sharing Arrangements

Employers and employees can establish various cost-sharing arrangements to determine the proportion of premiums each party will cover. Some common examples include:

- Employer pays a percentage of the premium while employees cover the rest

- Employees contribute a set amount each month towards the premium

- Costs are shared through deductibles, where employees pay a specified amount before insurance coverage kicks in

Effective Communication Strategies

Communicating with employees about their financial responsibilities in terms of health insurance contributions is crucial for transparency and understanding. Employers can implement the following strategies:

- Provide clear and detailed explanations of the cost-sharing arrangement

- Offer educational resources to help employees understand the impact of their contributions

- Encourage open dialogue and address any questions or concerns promptly

In conclusion, understanding the nuances of group health insurance costs is crucial for optimizing benefits while controlling expenses. By implementing strategic approaches and fostering transparent communication, organizations can create a win-win scenario for all parties involved.

{kind=link}