Family health coverage plans play a crucial role in safeguarding your loved ones’ well-being. From selecting the right plan to understanding key elements, this guide delves into everything you need to know.

Types of Family Health Coverage Plans

When it comes to family health coverage plans, there are various options available to suit different needs and preferences. Understanding the key features and benefits of each type can help families make informed decisions about their healthcare coverage.

Health Maintenance Organization (HMO)

- HMO plans typically require members to choose a primary care physician (PCP) and get referrals to see specialists.

- These plans often have lower out-of-pocket costs and focus on preventive care.

- Coverage is limited to a network of healthcare providers, and out-of-network care may not be covered except in emergencies.

Preferred Provider Organization (PPO)

- PPO plans offer more flexibility in choosing healthcare providers without a referral requirement.

- Members can see specialists without referrals but may pay higher out-of-pocket costs for out-of-network care.

- These plans provide coverage for both in-network and out-of-network services, giving families more options for healthcare providers.

Exclusive Provider Organization (EPO)

- EPO plans combine features of HMO and PPO plans, offering a network of healthcare providers without requiring referrals.

- Members must seek care within the network except in emergency situations.

- Out-of-network care is typically not covered, but EPO plans may have lower premiums compared to PPO plans.

High Deductible Health Plan (HDHP) with Health Savings Account (HSA)

- HDHPs have higher deductibles and lower premiums, paired with an HSA for tax-advantaged savings for medical expenses.

- Members can use HSA funds to pay for qualified healthcare expenses and save for future medical costs.

- These plans are suitable for families looking to save on premiums and take control of their healthcare spending.

Choosing the Right Family Health Coverage Plan

When it comes to selecting a family health coverage plan, there are several factors to consider to ensure you choose the right one for your family’s needs. Evaluating the suitability of a plan involves looking at various aspects to make an informed decision that provides the best coverage possible.

Factors to Consider

- Cost: Determine the monthly premiums, deductibles, copayments, and out-of-pocket maximums to understand the financial implications of the plan.

- Coverage: Evaluate the services covered, including doctor visits, hospital stays, prescription drugs, preventive care, and other essential healthcare needs.

- Network: Check if your preferred healthcare providers, hospitals, and specialists are included in the plan’s network to ensure you can access quality care.

- Benefits: Look at additional benefits offered, such as telemedicine, wellness programs, maternity care, mental health services, and vision or dental coverage.

- Flexibility: Consider the flexibility of the plan in terms of changing doctors, seeking care out-of-network, or adding dependents in the future.

Tip for Evaluation, Family health coverage plans

- Assess your family’s healthcare needs and priorities to match them with the plan’s coverage options effectively.

- Compare multiple plans from different insurers to find the one that offers the best value and meets your specific requirements.

- Read the plan documents carefully, including the summary of benefits and coverage, to understand the details and potential limitations.

- Seek guidance from a licensed insurance agent or healthcare navigator to clarify any doubts and get personalized recommendations.

Importance of Network Coverage

Network coverage plays a crucial role in the decision-making process when choosing a family health coverage plan. Having access to a wide network of healthcare providers ensures that you can receive care from professionals you trust without facing additional out-of-network costs. It also allows for coordinated and comprehensive care, especially if you have ongoing health conditions or require specialized treatments. Before enrolling in a plan, verify if your primary care physician, specialists, and preferred healthcare facilities are within the plan’s network to guarantee seamless healthcare delivery for you and your family.

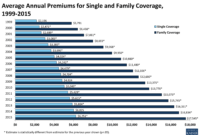

Understanding Premiums, Deductibles, and Co-payments

When considering family health coverage plans, it is essential to understand the key financial components that can impact your overall healthcare costs. Premiums, deductibles, and co-payments play a significant role in determining how much you will pay for healthcare services and coverage.

Premiums are the fixed amount you pay to your insurance provider on a regular basis, typically monthly, to maintain your health coverage. Deductibles refer to the amount you must pay out of pocket before your insurance starts covering the costs. Co-payments are set fees you pay for specific healthcare services, such as doctor visits or prescription medications, after you have met your deductible.

These factors can greatly influence your monthly expenses and overall healthcare costs for your family. Choosing higher premiums may result in lower out-of-pocket expenses for each healthcare service, while opting for a higher deductible could mean lower monthly premiums but higher costs when you actually need medical care. Co-payments also add to your expenses for each service you receive.

For example, a family with a higher premium plan may have lower out-of-pocket costs for doctor visits and medications, but they will pay more each month for their coverage. On the other hand, a family with a high-deductible plan may have lower monthly premiums but will need to cover a larger portion of their healthcare costs until they reach their deductible.

Understanding how premiums, deductibles, and co-payments work together is crucial in selecting the right family health coverage plan that meets your financial needs and healthcare requirements.

Coverage for Pre-Existing Conditions and Preventive Care

When it comes to family health coverage plans, handling pre-existing conditions and providing coverage for preventive care services are crucial aspects that can greatly impact the overall well-being of the insured individuals.

Coverage for Pre-Existing Conditions

Pre-existing conditions are medical conditions that existed before the start of a health insurance policy. Many family health coverage plans have provisions to cover pre-existing conditions, although the specifics can vary. It’s important to carefully review the policy to understand how pre-existing conditions are handled, including any waiting periods or limitations on coverage.

Common pre-existing conditions that may be covered by family health plans include diabetes, asthma, high blood pressure, and certain mental health disorders. These conditions require ongoing management and treatment, so having coverage for them is essential for maintaining good health.

Importance of Coverage for Preventive Care Services

Preventive care services are designed to help individuals stay healthy and detect any potential health issues early on. Many family health coverage plans include coverage for preventive services such as annual check-ups, vaccinations, screenings, and counseling. By promoting preventive care, insurance plans aim to prevent more serious health issues down the line and reduce healthcare costs in the long run.

Examples of Common Pre-Existing Conditions and Preventive Care Services Covered

- Pre-Existing Conditions:

- Diabetes

- Asthma

- High blood pressure

- Anxiety disorders

- Preventive Care Services:

- Annual physical exams

- Immunizations

- Cancer screenings

- Nutritional counseling

In conclusion, ensuring your family has the most suitable health coverage plan is paramount for their health and financial security. Make informed decisions based on the Artikeld factors to secure a better future for your loved ones.

When it comes to comparing health insurance plans online, it’s important to consider factors such as coverage, premiums, and deductibles. By visiting a trusted website like Compare health insurance plans online , you can easily compare different options and choose the one that best fits your needs.

Seniors have unique healthcare needs, which is why it’s crucial to find health insurance plans specifically tailored for them. Websites like Health insurance plans for seniors offer comprehensive information on coverage options and benefits for older individuals.

For those looking for top-rated health insurance companies, it’s essential to research and compare different providers. Websites like Top-rated health insurance companies provide insights into customer satisfaction, coverage options, and financial stability of various insurance companies.

{kind=link}