High deductible health plans (HDHP) sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with ahrefs author style and brimming with originality from the outset.

High deductible health plans (HDHP) are a crucial aspect of the healthcare industry, shaping how individuals approach their medical expenses and coverage. Understanding the key features, pros, cons, and impact of HDHPs is essential for making informed decisions regarding healthcare options.

Overview of High Deductible Health Plans (HDHP)

High Deductible Health Plans (HDHP) are a type of health insurance plan that requires individuals to pay a higher deductible before the insurance company starts covering medical expenses. These plans typically have lower monthly premiums but higher out-of-pocket costs.

Key features of HDHPs include a deductible that must be met before insurance coverage kicks in, as well as the ability to pair them with a Health Savings Account (HSA) for tax advantages. HDHPs also often cover preventive care services before the deductible is met.

The purpose of HDHPs in the healthcare industry is to encourage cost-conscious healthcare decision-making by individuals. By requiring higher out-of-pocket expenses, HDHPs aim to promote price transparency, reduce unnecessary medical expenses, and ultimately lower overall healthcare costs for both individuals and insurance providers.

Pros and Cons of High Deductible Health Plans

When considering High Deductible Health Plans (HDHP), it is essential to weigh the advantages and disadvantages to make an informed decision about your healthcare coverage.

Advantages of HDHP

- Lower Monthly Premiums: HDHPs typically have lower monthly premiums compared to traditional health insurance plans, making them an attractive option for individuals looking to save on costs.

- Tax Benefits: Contributions to a Health Savings Account (HSA) with an HDHP are tax-deductible, allowing for additional savings on healthcare expenses.

- Consumer Control: HDHPs empower individuals to take control of their healthcare spending by allowing them to choose when and where to seek medical care.

- Preventive Care Coverage: Many HDHPs cover preventive care services at no cost to the individual, promoting overall health and wellness.

Disadvantages of HDHP

- High Deductibles: The main drawback of HDHPs is the high deductible that must be met before the insurance coverage kicks in, which can lead to significant out-of-pocket expenses.

- Limited Coverage: HDHPs may offer limited coverage for certain services or treatments, requiring individuals to pay more for specialized care.

- Financial Strain: Meeting a high deductible can be financially challenging for individuals with chronic health conditions or unexpected medical emergencies.

- Risk of Delayed Care: Some individuals may delay necessary medical treatment due to concerns about meeting the high deductible, potentially leading to more severe health issues.

Comparison with Traditional Health Insurance Plans

- Cost Structure: HDHPs generally have lower monthly premiums but higher deductibles compared to traditional health insurance plans, offering a trade-off between upfront costs and out-of-pocket expenses.

- Flexibility: HDHPs provide more flexibility in managing healthcare expenses and choosing providers, while traditional plans may have more comprehensive coverage but less control for the individual.

- Health Savings Account: HDHPs are often paired with Health Savings Accounts (HSAs) to help individuals save for future medical expenses tax-free, providing a unique financial benefit not typically found in traditional plans.

- Risk Tolerance: Opting for an HDHP requires individuals to assess their risk tolerance for potential out-of-pocket costs, whereas traditional plans offer more predictable coverage but may come with higher monthly premiums.

Eligibility and Enrollment for HDHPs

When it comes to High Deductible Health Plans (HDHPs), understanding who is eligible and how individuals can enroll is crucial. Employers also play a key role in offering HDHPs as part of their benefits packages.

Eligibility for HDHPs

- Individuals who are not enrolled in Medicare and do not have coverage under another health plan are usually eligible for HDHPs.

- Typically, individuals need to meet certain deductible and out-of-pocket maximum requirements to qualify for an HDHP.

Enrollment Process for HDHPs

- Enrollment in an HDHP usually occurs during open enrollment periods, which are set by the employer or insurance provider.

- Individuals can also enroll in an HDHP within a specified period after experiencing a qualifying life event, such as marriage, birth of a child, or loss of other health coverage.

- Enrollment can often be done online through the employer’s benefits portal or by filling out a paper enrollment form.

Employer Offered HDHPs

- Employers may offer HDHPs as part of their benefits packages to provide employees with a more cost-effective option for healthcare coverage.

- Employers typically contribute to employees’ Health Savings Accounts (HSAs) to help offset the higher deductibles associated with HDHPs.

- Employees may have the option to choose between an HDHP and a traditional health plan during the open enrollment period.

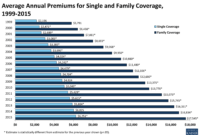

Cost and Coverage Details of HDHPs: High Deductible Health Plans (HDHP)

When considering a High Deductible Health Plan (HDHP), it is important to understand the typical costs involved and the coverage provided by these plans.

Costs of HDHPs

- HDHPs typically have lower monthly premiums compared to traditional health insurance plans.

- However, the deductibles for HDHPs are higher, meaning you will have to pay more out-of-pocket for medical expenses before the insurance coverage kicks in.

- There are also out-of-pocket maximums set by HDHPs, which limit the total amount you have to pay in a given year.

Coverage of HDHPs

- HDHPs cover preventive care services, such as annual check-ups, vaccinations, and screenings, at no cost to the insured.

- They also cover a range of medical services like hospital stays, emergency room visits, and prescription drugs, but you will have to meet the deductible first.

- Some HDHPs offer coverage for additional services like mental health care, maternity care, and rehabilitation services.

Relationship to HSAs and FSAs

- HDHPs are often paired with Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) to help individuals save for medical expenses.

- HSAs allow you to contribute pre-tax money to use for qualified medical expenses, and the funds roll over from year to year.

- FSAs are similar but have a “use it or lose it” rule, meaning you must use the funds within the plan year or forfeit them.

Impact of HDHPs on Healthcare Decisions

When it comes to High Deductible Health Plans (HDHPs), the impact on healthcare decisions is significant. Individuals enrolled in HDHPs often approach healthcare differently due to the unique financial structure of these plans.

Influence on Healthcare-Seeking Behaviors

- HDHPs tend to make individuals more cost-conscious when seeking medical care.

- Patients may delay or avoid non-urgent medical treatments to save on out-of-pocket costs.

- Individuals may opt for telemedicine or urgent care centers over traditional doctor visits to save money.

Role of Preventive Care in HDHPs

- Preventive care services are usually covered at no cost in HDHPs, encouraging individuals to prioritize regular check-ups and screenings.

- Early detection through preventive care can help individuals avoid more serious health issues in the future, potentially saving on overall healthcare costs.

- Some individuals may still skip preventive care due to concerns about high deductibles, leading to missed opportunities for early intervention.

Effect on the Overall Healthcare System, High deductible health plans (HDHP)

- HDHPs can create disparities in healthcare access, as individuals with lower incomes may struggle to afford out-of-pocket costs for necessary treatments.

- Healthcare providers may see changes in patient volume and types of services sought, as individuals with HDHPs may be more selective in their healthcare utilization.

- The overall cost of healthcare delivery may be influenced by the prevalence of HDHPs, as shifts in patient behaviors can impact provider revenues and healthcare spending trends.

In conclusion, High deductible health plans (HDHP) present a unique approach to healthcare coverage, balancing advantages and challenges while influencing individuals’ healthcare decisions. By exploring the intricacies of HDHPs, individuals can navigate the healthcare landscape more effectively, taking control of their medical expenses and choices.

{kind=link}