Health insurance for self-employed individuals is a crucial aspect of financial planning. From understanding the basics to navigating the Affordable Care Act, this guide covers everything you need to know to make informed decisions about your healthcare coverage.

When it comes to choosing the right plan and managing costs effectively, self-employed individuals face unique challenges that require careful consideration and strategic planning.

Understanding Health Insurance for Self-Employed Individuals

Health insurance is a type of coverage that helps individuals pay for medical expenses by spreading the risk across a pool of policyholders. It is crucial for self-employed individuals to have health insurance to protect themselves from high medical costs and ensure access to necessary healthcare services.

Health Insurance Options for Self-Employed Individuals, Health insurance for self-employed individuals

Self-employed individuals have several options for health insurance coverage. They can choose between individual health insurance plans or group health insurance plans.

- Individual Health Insurance: Self-employed individuals can purchase individual health insurance plans directly from insurance companies or through the Health Insurance Marketplace. These plans offer coverage for the individual and their family members, with premiums based on factors like age, location, and coverage level.

- Group Health Insurance: Self-employed individuals may also be eligible to join group health insurance plans through professional associations, chambers of commerce, or other organizations. Group health insurance plans typically offer lower premiums and more comprehensive coverage compared to individual plans.

It is important for self-employed individuals to carefully compare the benefits, costs, and coverage options of individual and group health insurance plans to choose the best option for their needs.

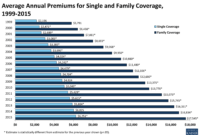

Factors to Consider When Choosing Health Insurance: Health Insurance For Self-employed Individuals

When choosing health insurance as a self-employed individual, there are several key factors to consider to ensure you select a plan that meets your needs and budget. Factors such as premiums, deductibles, out-of-pocket costs, coverage options, network providers, and prescription drug coverage all play a significant role in determining the suitability of a health insurance plan.

Impact of Premiums, Deductibles, and Out-of-Pocket Costs

- Premiums: Premiums are the monthly payments you make to maintain your health insurance coverage. It’s essential to consider how much you can afford to pay each month without straining your budget.

- Deductibles: Deductibles are the amount you must pay out of pocket before your insurance coverage kicks in. Higher deductibles typically result in lower monthly premiums but may require you to pay more upfront for medical expenses.

- Out-of-Pocket Costs: These include expenses such as copayments, coinsurance, and any costs not covered by your insurance plan. Understanding these costs can help you estimate your total healthcare expenses throughout the year.

Comparison of Coverage Options, Network Providers, and Prescription Drug Coverage

- Coverage Options: Different health insurance plans offer varying levels of coverage, including services like doctor visits, hospital stays, preventive care, and maternity care. Make sure the plan you choose aligns with your healthcare needs.

- Network Providers: Consider whether your preferred healthcare providers, such as doctors and specialists, are included in the plan’s network. Out-of-network providers may result in higher out-of-pocket costs.

- Prescription Drug Coverage: If you take prescription medications regularly, ensure that the health insurance plan provides adequate coverage for your prescriptions. Check the formulary to see if your medications are covered and at what cost.

Affordable Care Act (ACA) and Health Insurance for Self-Employed

The Affordable Care Act (ACA) has had a significant impact on health insurance options for self-employed individuals. It has introduced several provisions aimed at making health insurance more accessible and affordable for this demographic.

Subsidies and Tax Credits

- The ACA offers subsidies to help lower the cost of health insurance premiums for self-employed individuals. These subsidies are based on income and help make coverage more affordable.

- Self-employed individuals may also be eligible for tax credits under the ACA. These credits can further reduce the cost of health insurance premiums, making coverage more financially feasible.

- By taking advantage of these subsidies and tax credits, self-employed individuals can access quality health insurance coverage at a more affordable price.

Individual Mandate

- The individual mandate under the ACA requires all individuals to have health insurance coverage or face a penalty. This mandate has implications for self-employed individuals who must ensure they have adequate coverage to comply with the law.

- Self-employed individuals can purchase health insurance through the Health Insurance Marketplace established by the ACA to find a plan that meets their needs and satisfies the individual mandate.

- Failure to have health insurance coverage may result in a penalty when filing taxes, so it’s essential for self-employed individuals to understand their obligations under the individual mandate.

Tips for Managing Health Insurance Costs as a Self-Employed Individual

When you are self-employed, managing health insurance costs is crucial to ensure you have adequate coverage without breaking the bank. Here are some strategies to help you navigate the complex world of health insurance and keep costs in check.

Importance of Budgeting and Planning

One of the first steps in managing health insurance costs as a self-employed individual is to create a budget specifically for healthcare expenses. By planning ahead and setting aside funds for premiums, deductibles, and out-of-pocket costs, you can avoid financial surprises and ensure that you can afford the coverage you need.

Negotiating with Insurance Providers

Don’t be afraid to negotiate with insurance providers to get the best possible rates. In some cases, you may be able to lower your premiums by opting for a higher deductible or exploring different coverage options. It’s also worth shopping around and comparing quotes from multiple providers to ensure you are getting the most competitive rates.

Leveraging Professional Associations

Professional associations or industry groups often have group health insurance plans that are available to self-employed individuals. By joining these organizations, you may be able to access more affordable coverage options that are typically only available to larger groups. This can help you save money on premiums and other healthcare costs.

In conclusion, prioritizing your health insurance as a self-employed individual is key to safeguarding your well-being and financial stability. By understanding the available options and implementing cost-saving strategies, you can ensure comprehensive coverage without breaking the bank.

{kind=link}